Public OOH Valuations March 2026

Welcome to the monthly Public OOH Valuations report. Each month, this segment breaks down the financials of the largest publicly traded out-of-home companies in the U.S. — stock prices, EBITDA multiples, leverage, and whether the market is pricing them right.

This month covers all three: Lamar Advertising (LAMR), OUTFRONT Media (OUT), and Clear Channel Outdoor (CCO).

Note: This is the first and final month covering CCO. Mubadala Capital's $6.2 billion take-private deal is expected to close in Q3 2026, after which CCO will delist. There are no other publicly traded pure-play OOH companies in the U.S., so future installments will cover LAMR and OUT only.

What Happened This Month

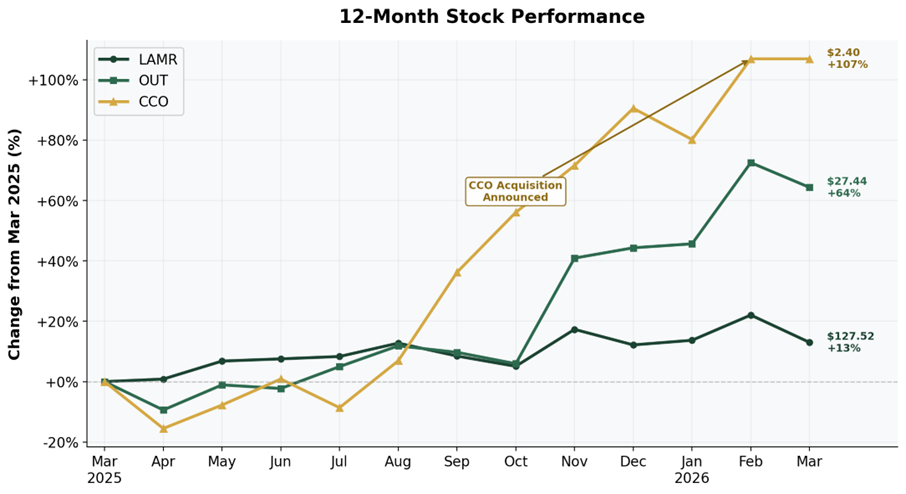

- The dominant story: Clear Channel's take-private deal. On February 9, Mubadala Capital and TWG Global agreed to acquire CCO for $6.2 billion in enterprise value — $2.43 per share in cash, a 71% premium to the unaffected share price of $1.42. There is a 45-day go-shop period that expires March 26 with no competing bid reported. The deal is expected to close by the end of Q3 2026.

- Lamar's CEO Sean Reilly spoke at the Morgan Stanley TMT Conference on March 4. Key points: Targeting an EBITDA margin target of 48%+ by 2028, $65 million in digital conversions this year, $150–200 million in tuck-in acquisitions, and ~10% programmatic growth expected in 2026.

- OUTFRONT reported Q4 2025 results on February 26, beating AFFO estimates. Transit revenue jumped 16% year-over-year. Digital revenue mix hit 39% of total. Management guided for double-digit AFFO growth in 2026 and high-single-digit revenue growth in Q1. The strong guidance and transit momentum largely explain OUT's run from ~$16 to $27+ over the past year.

Lamar Advertising (LAMR) — $127.52

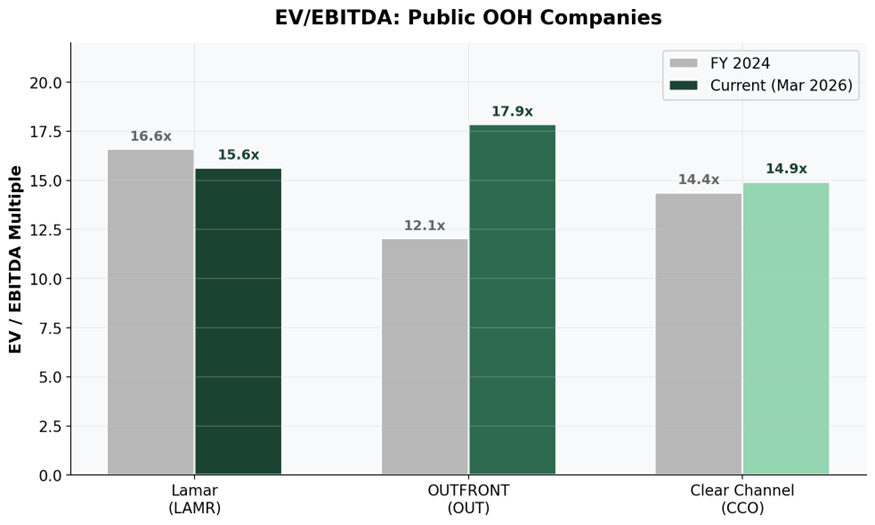

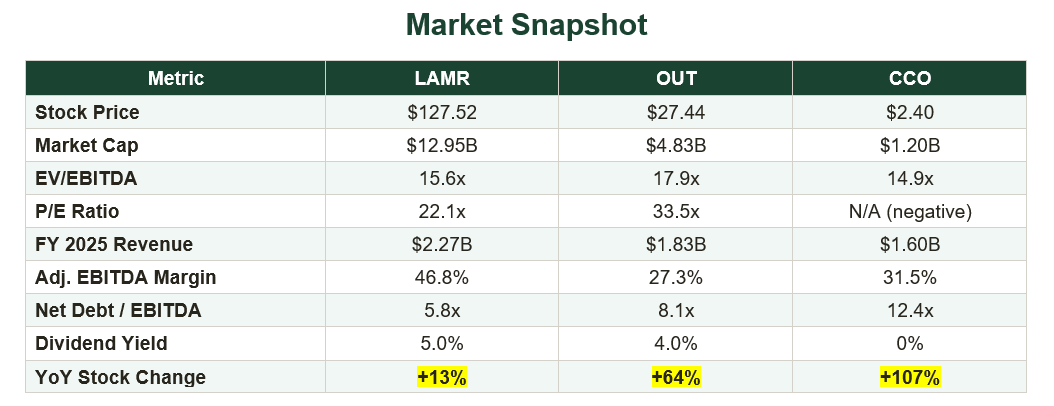

Trading at 15.6x EV/EBITDA, below last year's 16.6x and in line with its five-year average around 15x. Up 13% year-over-year — steady, no single catalyst. CEO Sean Reilly laid out the roadmap at the Morgan Stanley TMT Conference in early March: 48%+ EBITDA margin target by 2028, $65 million in digital conversions this year, $150–200 million in tuck-in acquisitions, and ~10% programmatic growth. Paying ~$6.46/share in dividends (5.0% yield).

OUTFRONT Media (OUT) — $27.44

Up 64% year-over-year, from $16.70 to $27.44. The re-rating started in November after Q4 results showed transit revenue up 16% and an AFFO beat. Management guided for double-digit AFFO growth in 2026. That move pushed EV/EBITDA to 17.9x — well above last year's 12.0x and the historical average around 14x. Digital revenue mix now at 39%.

Clear Channel Outdoor (CCO) — $2.40 [Final Month]

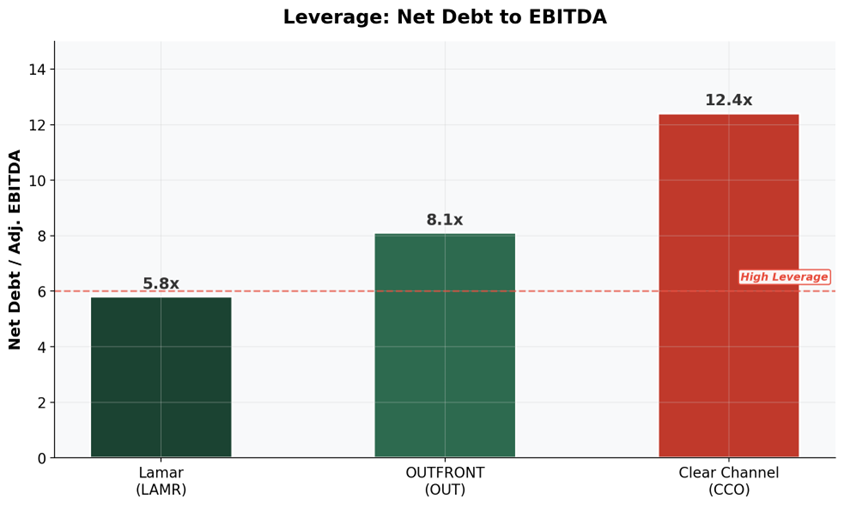

Final month for CCO. Mubadala Capital's $6.2 billion take-private ($2.43/share, 71% premium) is expected to close Q3 2026. Stock is at $2.40 — pennies below the deal price, up 107% YoY on buyout speculation. The acquisition values CCO at 12.3x EV/Adjusted EBITDA, a discount to both LAMR and OUT, justified by 12.4x leverage and -$3.4 billion in stockholders' equity. Go-shop expiring March 26 with no competing bid present.

Billboard Economics' Take

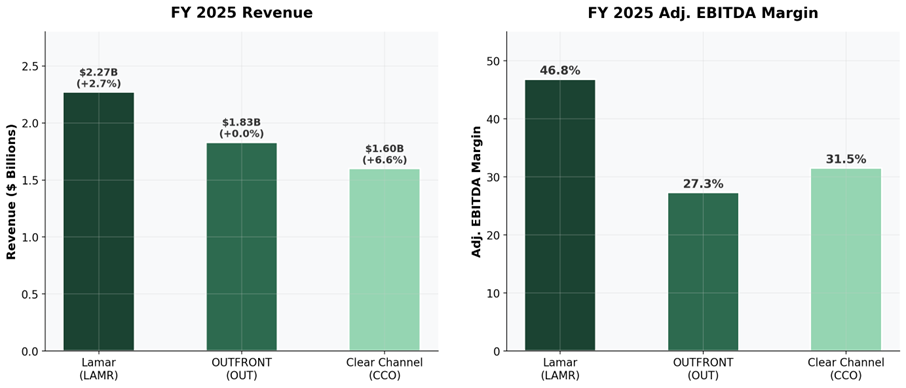

Lamar is Lamar. 15.6x, 46.8% margin, steady as always. Multiple came down slightly from last year even with earnings growth.

OUTFRONT had a big year. Transit came back, digital mix hit 39%, and the stock re-rated hard. Whether 17.9x holds depends on the revenue line catching up to the multiple.

CCO going private at 12.3x EBITDA tells you something. Mubadala looked past a rough balance sheet and paid $6.2 billion for the assets underneath it.

Some Interesting Graphs Below:

You can subscribe for free by entering your email below. Our newsletter is free.