Billboard Cashflow vs EBITDA: What metric to use when valuing your billboards

If you ask most business brokers how to value a company, they’ll talk about a multiple of EBITDA. EBITDA is fine for comparing generic businesses, but it bakes in how you choose to run the operation.

In out-of-home, billboards are valued on a multiple of billboard cash flow (BCF) instead of EBITDA. Since an acquirer will roll your faces into their existing SG&A, they care about what the boards produce on a pure cash basis, not the expenses you might incur to your specific plant. Costs like office expenses, owner salary, etc., will not be assumed in the new buyer's operation.

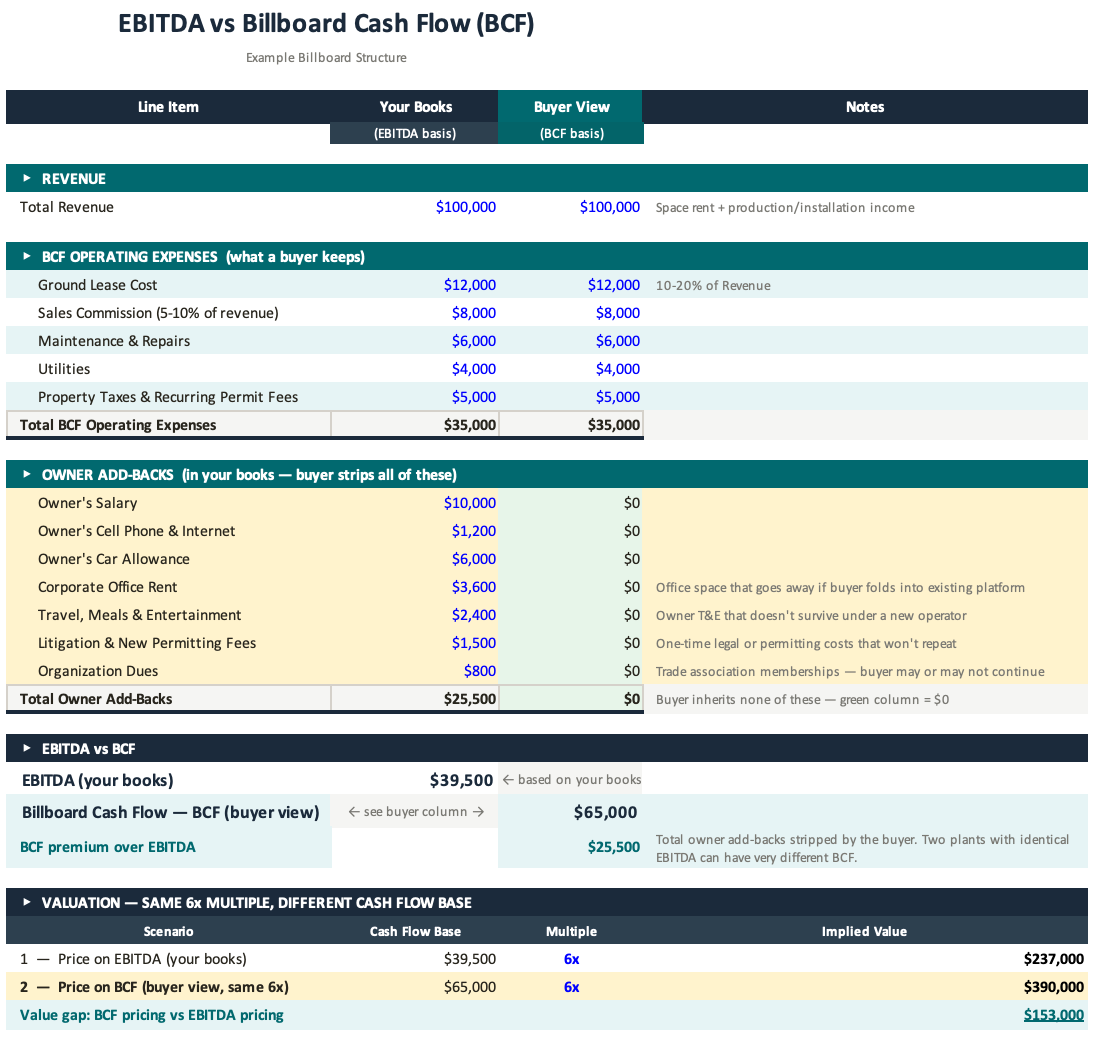

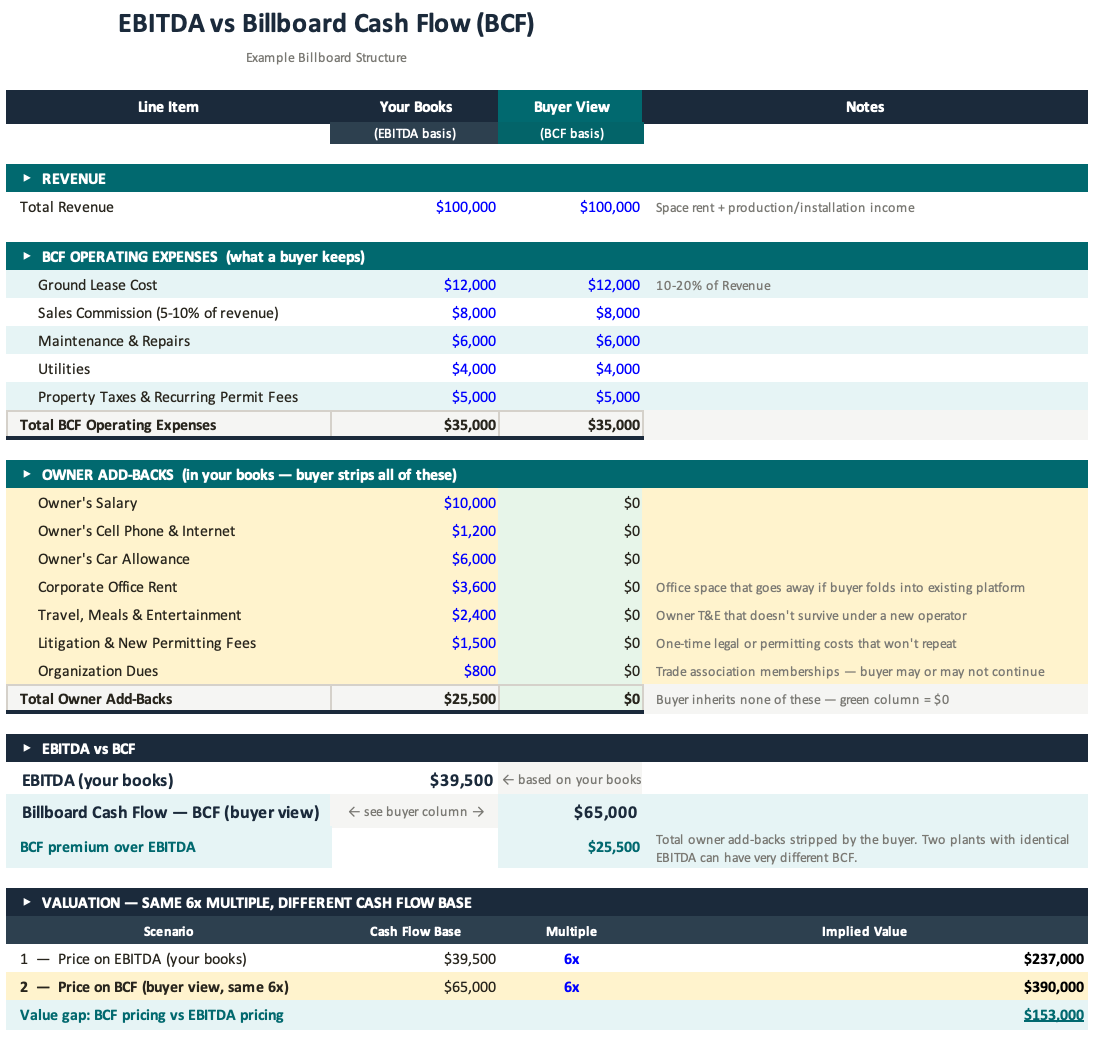

EBITDA vs Billboard Cash Flow (BCF)

EBITDA includes:

- office rent

- admin staff

- sales salaries and commissions

- owner compensation

Those costs vary widely between operators. Two companies can own identical billboards and show completely different EBITDA margins based on how they run their business. That makes EBITDA less useful when you are trying to value the underlying asset.

BCF strips that out.

It focuses on the direct economics of each board itself:

- revenue (space + production)

- - ground lease cost

- - implied sales commission (5–10% of revenue)

- - maintenance and repairs

- - utilities

- - property taxes and recurring permit fees

= BCF

How This Can Affect Your Valuation

See the example model below:

Using the same 6x multiple, the difference comes entirely from the cash flow base being used.

- 6x EBITDA ($39,500) → $237,000

- 6x BCF ($65,000) → $390,000

That’s a $153,000 value gap on the same board.

This is a simple example, but it highlights how two identical boards can produce very different valuations depending on how they’re viewed.

Let me know your thoughts below!